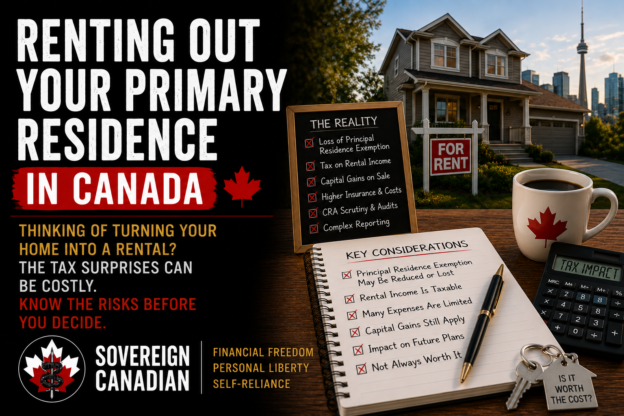

The kids are gone. The cottage covers the summers. Somewhere warm covers the winters. And the family home sits there, mostly or completely paid off, quietly worth more than anything else you own. Do you sell it and invest the proceeds — or keep it and turn it into a rental? Here’s what actually happens when you do the second thing, and why the tax consequences run deeper than the income line.

Continue reading