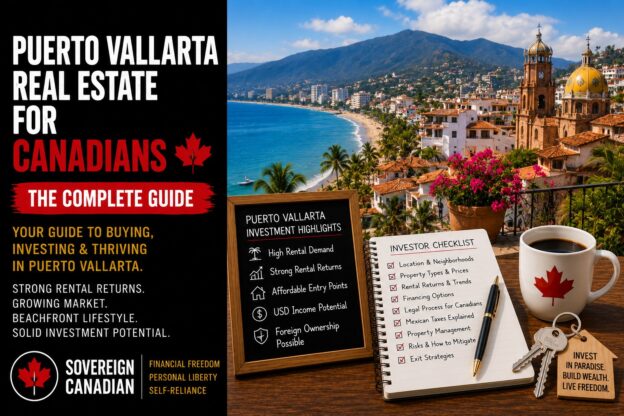

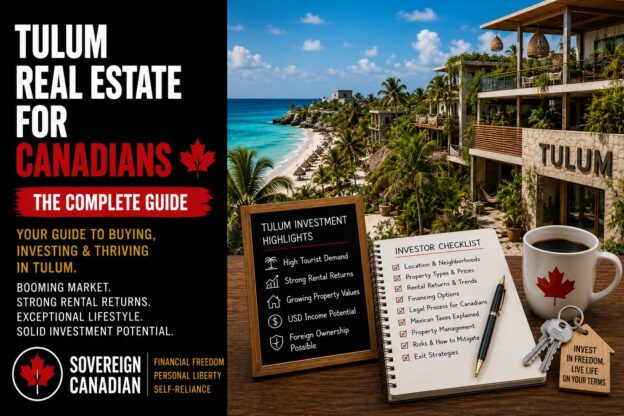

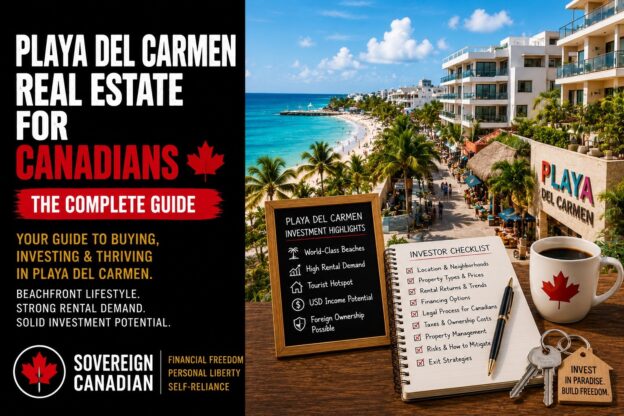

Mexico comes up constantly when Canadians start talking about buying abroad. It’s close, it’s cheap relative to home, the weather solves your February problem, and half the country seems to already have a cousin with a condo in Puerto Vallarta. But “close and cheap” isn’t a strategy — and Mexico has enough legal quirks, financing friction, and rental-market nuance that showing up with vibes and a vague sense that “Mexican real estate is a good deal” will get you into trouble.

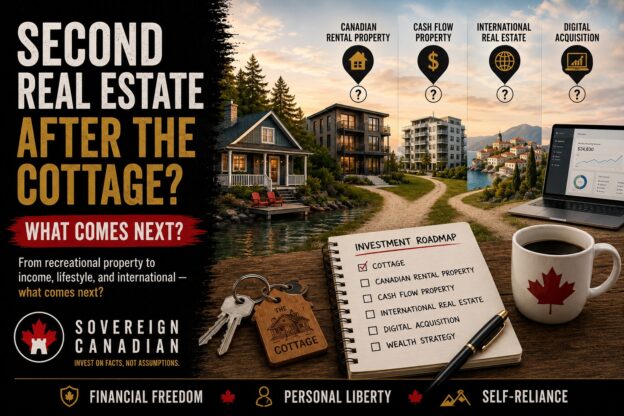

This post is the primer. It won’t make you an expert on any single market — Riviera Maya, Puerto Vallarta, and Mérida each deserve their own deep dive, and those are coming. What it will do is give you the framework: where Canadians actually buy and why, how ownership legally works, how financing really functions (spoiler: not the way you’re used to), and the practical difference between running a short-term rental and a long-term one. By the end, you’ll know enough to ask the right questions instead of the obvious ones. Mexico is one of the locations I’m thinking of for a next investment.

Continue reading →